AI Data Center Construction Boom

AI Data Centers: A $400bn – $750bn Opportunity by 2030

Date: 9th February 2026

Global technology is shifting from general cloud computing to high-density AI infrastructure, marking a “trillion-dollar” era where the megawatt (MW) has become the primary metric of value. Driven by the extreme power demands of next-generation accelerators like Nvidia’s Blackwell and Rubin, this transition requires a fundamental re-engineering of physical data centers. This report analyzes the construction economics, regional dynamics, and systemic risks associated with deploying these critical 100MW AI facilities.

In our previous post, we discussed the massive ongoing build-out of AI infrastructure. In that analysis, we excluded AI data center construction costs from our ‘Industry Model’ due to the scarcity of publicly available information. Furthermore, the prevalence of operating and finance lease structures obfuscates the total quantum of investment in AI data centers.

Prior to the proliferation of Nvidia’s AI GPUs, a general server typically housed two CPUs per tray, consuming 1kW of power. In contrast, an AI server tray houses two CPUs and eight Nvidia AI GPUs, consuming 10kW. This drastic increase renders most existing data centers incapable of powering the latest AI hardware.

The Megawatt as the New Unit of Value: Global Construction Economics

In the contemporary data center market, the “megawatt” has evolved beyond a mere measure of electrical consumption to become a comprehensive benchmark for construction costs, land utilization, and technological maturity. Historically, data center development was measured by square footage (acres or hectares of development), but the emergence of AI workloads has rendered spatial metrics secondary to power density. Modern AI clusters demand massive electrical and thermal infrastructure that occupies less physical space per unit of compute than traditional servers but requires significantly more investment in the “warm shell” and power subsystems.

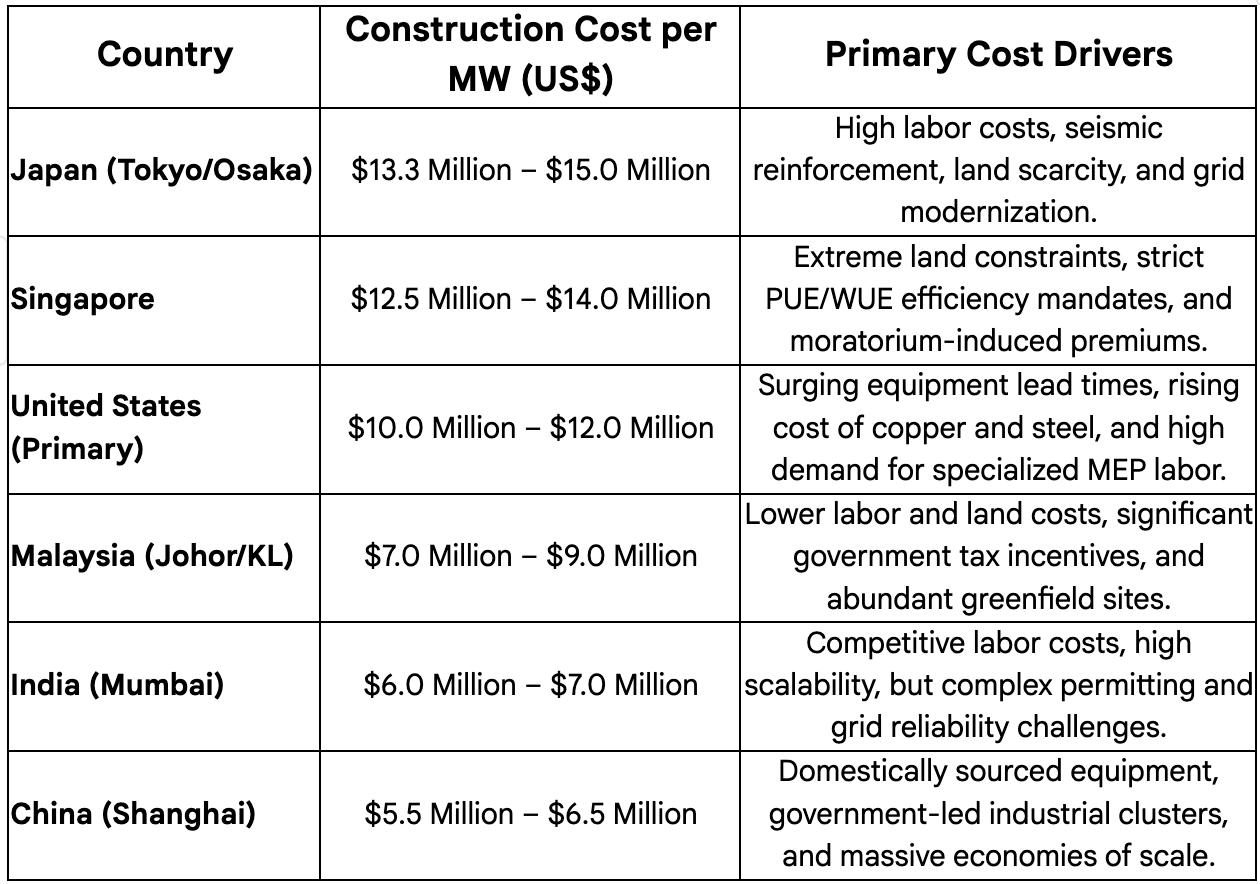

Regional Cost Benchmarks per Megawatt

The capital expenditure required to construct a data center shell—including the physical building, high-voltage electrical distribution, and advanced cooling systems—varies dramatically across global hubs. These variations are driven by labor markets, regulatory frameworks, seismic requirements, and the maturity of the local power grid.

Exhibit 2: Estimated AI Data Center Cost of Construction

Source: Various news sources, company disclosures and public filings.

How Much Does it Cost to Build 40GW to 50GW of AI Data Center?

In our first post regarding the power demand from the massive AI infrastructure build-out—based on Nvidia’s reported data center revenue since 2023 and Jensen’s public comments on the company’s order backlog—our industry model excluded the capital investments required to power this global infrastructure.

In this post, we estimate the total construction cost of building the dedicated AI data centers necessary to support the infrastructure running today’s widely used AI applications.

Key Assumptions:

We use US$10 million - US$15 million as the lower and upper range per MW of AI Data Center capacity.

A standard AI cluster houses 100MW, enough to fit 100,000 Nvidia’s AI GPU to perform large scale Large Language Model (LLM) training.

Cost of Construction for 100MW of AI Data Center:

In developing countries like Malaysia, it costs approximately US$1 billion (US$10 million x 100 MW) to build an AI data center ‘shell,’ excluding the cost of AI servers.

While some public filings or news reports may point to costs slightly lower than our US$10 million per MW assumption, it is worth noting that AI data centers built in 2023 benefited from lower costs as early builders quickly secured land with excess power capacity. This is no longer the case today.

Conversely, in developed countries like Japan—where certified construction workers are in short supply, strict government regulations govern building structure (seismic isolation system) and work practices—the cost per MW sits at the top end of the curve: US$15 million per MW, or US$1.5 billion per 100 MW AI Data Center.

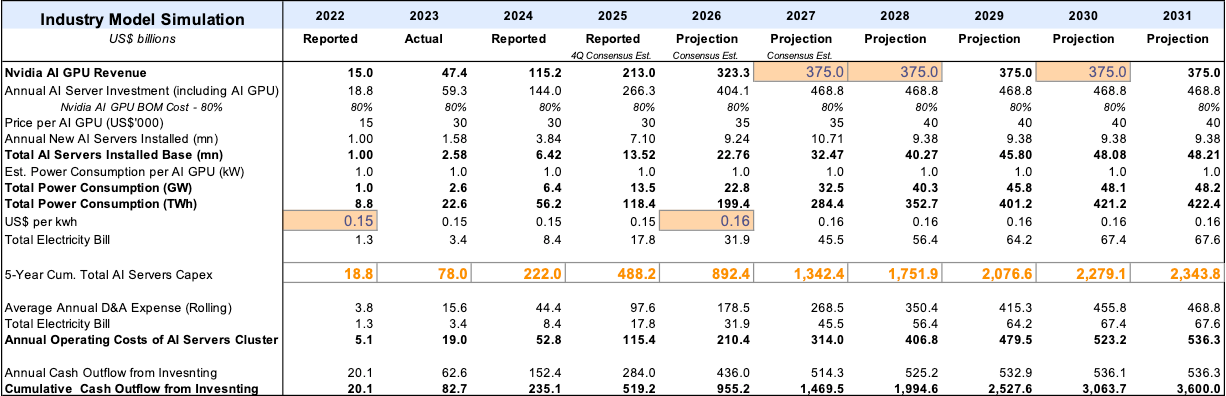

Based on our ‘Industry Model,’ the power demand for dedicated AI data centers required to support all Nvidia AI servers sold by the end of 2025 is roughly 13.52 GW. When including AI ASICs, AMD MI300/MI400 accelerators, and other custom silicon, the total power demand for AI servers is estimated at approximately 15 GW, assuming Nvidia maintains a >90% global market share.

Looking ahead to 2027 and 2028, power demand is projected to more than triple, reaching 33 GW and 40 GW, respectively. This projection is underpinned by Nvidia’s publicly disclosed order backlog ($500bn over 2 years) and corroborated by TSMC’s massive capital expenditure plans to expand capacity.

The capital expenditure for 40 GW – 50 GW of AI data centers is estimated between US$400billion and US$750 billion, spread over a 10 year period.

Exhibit 2: Global AI Compute Investment - 40GW to 50GW Demand by 2028/2031

Source: The Trillion Dollar AI Infrastructure Build-out; https://substack.com/home/post/p-186952576

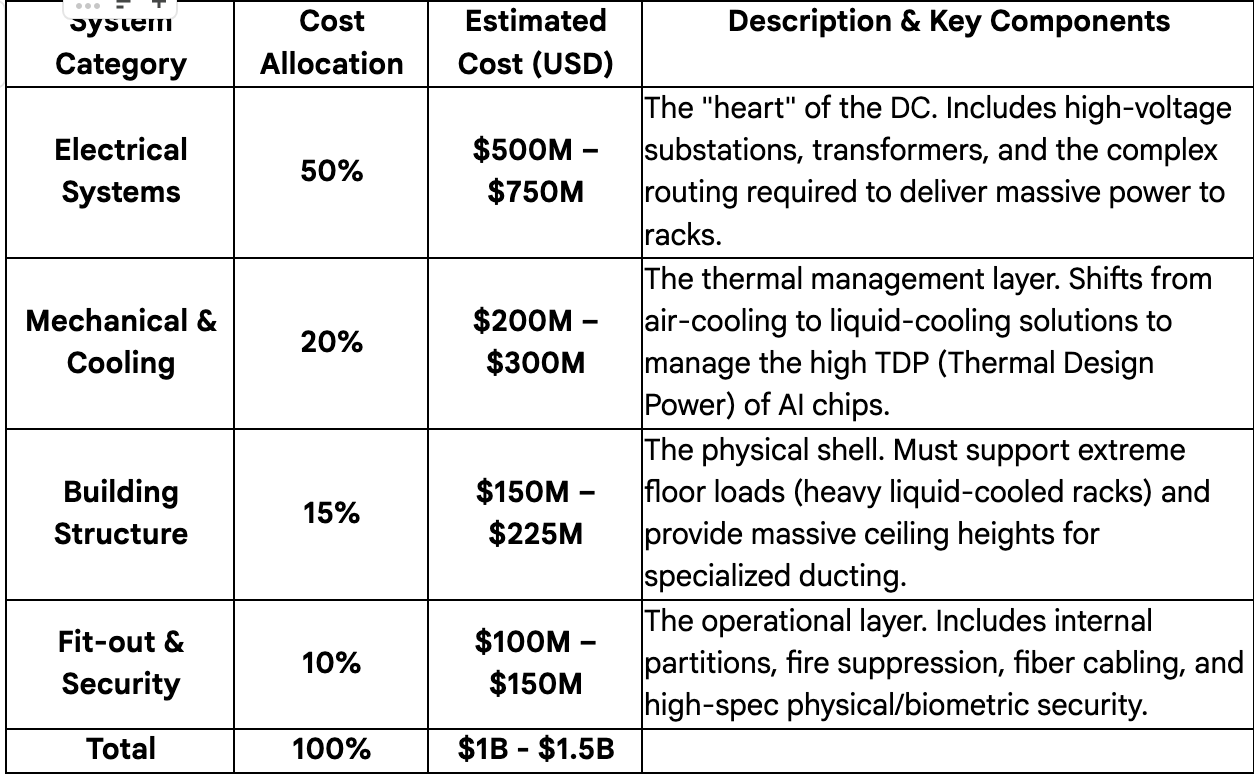

Dissecting the 100MW AI Data Center Cost Components

A 100MW facility represents the current “sweet spot” for large-scale AI training clusters. To house 100,000 high-end GPUs—assuming each unit, including its share of the host server, networking fabric, and storage, draws approximately 1kW—the data center must be engineered with extreme thermal and electrical tolerance.

Exhibit 3: Estimated Breakdown of AI Data Center Cost Components

Source: Various news sources, company disclosures and public filings.

Deep Dive: Systems & Critical Components

In this architecture, the electrical subsystem is the dominant cost driver, accounting for roughly half of the build. This includes transformers, redundant high-voltage substations, massive uninterruptible power supply (UPS) arrays using advanced chemistries like nickel-zinc or sodium-ion, and extensive backup generator capacity. For AI-ready facilities, the mechanical cooling budget is also shifting. As heat loads exceed 100kW, traditional air cooling is replaced by direct-to-chip liquid cooling or rear-door heat exchangers (RDHx), adding significant complexity to the piping and hydraulic infrastructure (mechanical & cooling).

1. Electrical Systems (The Power Path)

The priority here is redundancy and density. AI workloads cannot afford a millisecond of downtime, as a power blip could crash a multi-week training model.

Substation & Transformers: Converts utility high-voltage power to usable levels.

Critical Component - Dual Utility Feeds: Every Tier III or IV data center utilizes two independent power supply lines. If one grid segment fails, the other is already live.

Critical Component - Automatic Transfer Switch (ATS) & Static Transfer Switch (STS): An STS is particularly critical for AI; it can switch power sources in under 4 to 8 milliseconds, which is faster than the power supply of an AI server takes to drop its load.

Uninterruptible Power Supply (UPS): Large battery arrays (often Lithium-ion) that bridge the gap between a power failure and the diesel generators kicking in.

2. Mechanical & Cooling (Heat Dissipation)

AI servers generate intense heat. If the copper wiring and chips aren’t cooled, electrical resistance increases, leading to “thermal throttling” or hardware failure.

Chillers & Cooling Towers: Large-scale units that reject heat from the building to the outside environment.

Critical Component: Coolant Distribution Units (CDUs): In AI DCs, we often use Liquid-to-Liquid cooling. The CDU manages the pressure and flow of coolant directly to the “Cold Plates” sitting on top of the GPUs.

Wire & Cable Management: High-density power cables generate their own heat. Advanced DCs use active airflow or liquid-cooled busways to “cool down the copper wire” and prevent insulation degradation over long operating cycles.

3. Building Structure (The Shell)

Reinforced Flooring: A single AI rack can weigh over 3,000 lbs. The concrete slabs must be rated for extreme point-loading.

Increased Clear Heights: Required to accommodate the massive “Blue Hose” liquid cooling manifolds and heavy-duty overhead power busway systems.

4. Fit-out & Security (The Shell Completion)

Fire Suppression: Uses “Pre-action” dry pipe or gaseous systems that extinguish fires without damaging sensitive electronics with water.

Structured Cabling: Thousands of miles of high-speed InfiniBand or Ethernet fiber-optics to interconnect the AI nodes.

Exhibit 4: Microsoft’s New Fairwater AI Datacenter in Wisconsin

Source: Official Microsoft Blog, “Inside the world’s most powerful AI datacenter”

https://blogs.microsoft.com/blog/2025/09/18/inside-the-worlds-most-powerful-ai-datacenter/

Wisconsin’s Fairwater AI data center represents a monumental engineering achievement, occupying a 315-acre campus with 1.2 million square feet of capacity across three main structures. The project’s sheer scale is defined by its material intensity: the facility sits atop 46.6 miles of deep foundation piles and is framed by 26.5 million pounds of structural steel. Its utility infrastructure is equally massive, utilizing 120 miles of medium-voltage cabling and 72.6 miles of mechanical piping.

Exhibit 5: High Density Cluster of AI Infrastructure Servers

Source: Official Microsoft Blog, “Inside the world’s most powerful AI datacenter”

https://blogs.microsoft.com/blog/2025/09/18/inside-the-worlds-most-powerful-ai-datacenter/

Case Study: The YTL Power (Malaysia Power Generation Company) and Nvidia

The joint venture (JV) between YTL Power International and Nvidia marks a pioneering milestone in the global AI infrastructure landscape. As one of the first partners globally to deploy Nvidia’s cutting-edge GB200 NVL72 systems, YTL Power serves as a blueprint for how utility and infrastructure conglomerates can pivot into the “sovereign AI” space. This collaboration is not merely about hosting servers; it represents a strategic shift where national infrastructure players become the custodians of their country’s AI computing power.

The total collaboration value for this project in Johor is estimated at RM 10 billion (approximately US$2.36 - $2.38 billion).

Data Center Shell and Power Infrastructure: US$1.2 Billion (RM 5.1 Billion).

AI Hardware (Nvidia Blackwell NVL72 Racks): US$1.16 Billion - US$1.18 Billion (RM 4.9 Billion).

This breakdown reveals an infrastructure-to-hardware ratio of roughly 1:1, which is higher than the global average. This is explained by the project’s unique requirements: YTL is constructing a massive 500MW on-site solar plant to provide dedicated renewable energy to the facility.

When the cost of the solar farm and specialized liquid-cooling infrastructure for the Nvidia Blackwell chips is factored into the “shell” budget, the infrastructure investment reaches $12 million per MW—putting Johor’s most advanced facility on par with U.S. construction costs but with a much lower long-term carbon and energy price profile. And, it is self-sustaining.

Regional Parallels: The Indosat-Nvidia Partnership

A strikingly similar “Sovereign AI” model is emerging in Indonesia, where Nvidia has partnered with Indosat Ooredoo Hutchison to build an AI center in Surakarta (Central Java).

Similar Strategy: Just as YTL leverages its utility background, Indosat is pivoting from a traditional telco to an “AI-native” TechCo, aiming to build Indonesia’s sovereign AI infrastructure.

Investment Scale: The initial investment is projected at US$200 million, with plans to integrate Nvidia’s Blackwell architecture to support local enterprise and government workloads.

Strategic Goal: Both the YTL and Indosat deals underscore Nvidia’s strategy of partnering with national champions (utilities and telcos) to bypass traditional cloud providers, effectively creating a decentralized network of “AI Factories” embedded within local power and data grids.

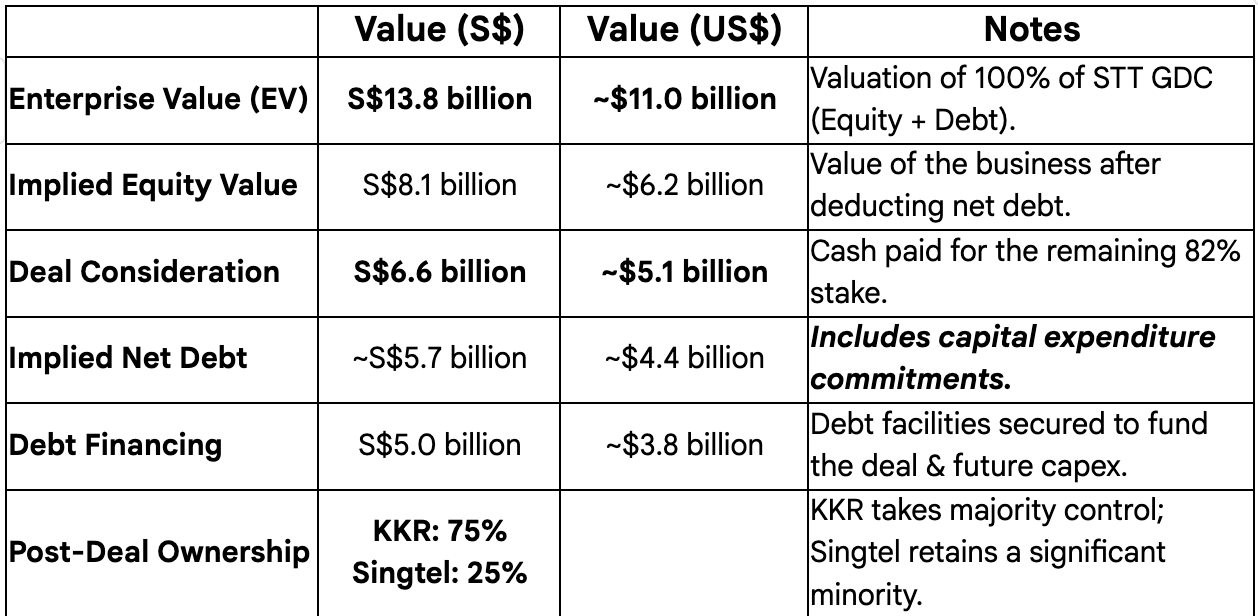

Case Study 2: KKR & Singtel’s Acquisition of STT GDC

On February 4, 2026, KKR and Singtel announced a landmark deal to acquire the remaining stake in ST Telemedia Global Data Centres (STT GDC), cementing one of the largest digital infrastructure transactions in Southeast Asia.

Key Details of the Acquisition:

1. Deal Structure & Valuation

The Buyers: A consortium led by KKR (taking a majority lead) and Singtel.

The Target: The remaining 82% stake in STT GDC (the consortium had previously invested ~S$1.75 billion in 2024 for a minority stake).

Purchase Price: S$6.6 billion (approx. US$5.1 billion) for the 82% stake.

Implied Enterprise Value: S$13.8 billion (approx. US$11 billion), including debt and capital expenditure commitments.

2. New Ownership Split

Upon completion (expected early second half of 2026), the ownership of STT GDC will be:

KKR: 75%

Singtel: 25%

(Note: This split accounts for the conversion of redeemable preference shares held by both parties from their 2024 investment.)

3. Strategic Rationale

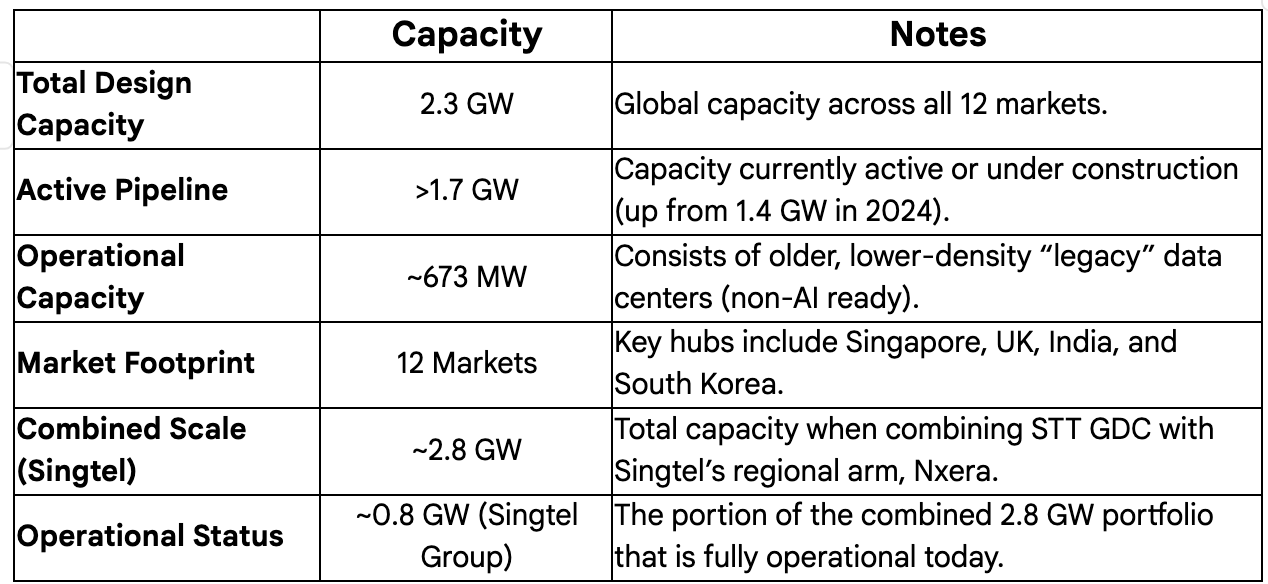

AI & Cloud Boom: The deal is explicitly driven by the “trillion-dollar” shift toward AI-ready infrastructure. STT GDC operates over 2.3GW of capacity across 12 markets (including key hubs in Singapore, the UK, India, and South Korea), positioning it to capture the massive demand from hyperscalers deploying GPU clusters.

Singtel’s “Singtel28” Plan: For Singtel, this is a major execution of its growth strategy to pivot from a traditional telco to a digital infrastructure powerhouse. It allows them to gain immediate global scale without shouldering the entire balance sheet burden alone.

Synergy with Nxera: Singtel already has a regional data center arm called Nxera (in which KKR also holds a 20% stake). This acquisition is separate but complementary, giving Singtel a dual-engine approach: Nxera for regional/integrated connectivity and STT GDC for massive global scale.

4. Market Context

“Sovereign AI” & Infrastructure: This deal mirrors the trend (like YTL/Nvidia) of major infrastructure funds and national telcos teaming up to own the physical layer of the AI economy.

Expansion: STT GDC has grown its pipeline significantly since the initial KKR investment, expanding from 1.4GW to over 1.7GW of active/under-construction capacity in just over a year.

Transaction Financials

Source: Public filings, news sources.

2. Operating Data & Portfolio Scale

Source: Public filings, news sources.

The acquisition values STT GDC at US$6.5 million per MW, factoring in the “legacy” data centers (~30% of total design capacity) and some discount to the “under construction” of 1.7 GW active pipeline.

Concluding Remarks:

The data center industry is undergoing a fundamental and rapid transformation driven by the extreme power and cooling demands of AI. This global shift marks the beginning of a “trillion-dollar” era, with construction and investment activities defined by three core dynamics:

1. The Megawatt as the New Unit of Value

Massive Capital Expenditure: Investment has transitioned from being measured by physical space (square footage) to power capacity (megawatt). AI data centers, which cost an estimated $10 million to $15 million per MW to construct, are driving a massive capital cycle, with projected power demand for dedicated AI servers alone reaching 40GW to 50GW by 2028/2031.

Engineering Redefinition: The construction cost is dominated by Electrical Systems (approx. 50% of the total) and advanced Mechanical & Cooling Systems (approx. 20%). This reflects a necessary engineering pivot away from traditional air-cooling to complex liquid-cooling solutions and high-redundancy power paths (like Static Transfer Switches and massive UPS arrays) to support the power density of modern AI accelerators.

2. Rise of Sovereign AI and Strategic Partnerships

Infrastructure-to-Hardware Alignment: The investment is characterized by strategic alliances between major chip providers (like Nvidia) and national infrastructure entities (like YTL Power in Malaysia and Indosat in Indonesia). This “Sovereign AI” model embeds dedicated “AI Factories” within local power and data grids, ensuring national control over critical AI compute capacity.

High-Value M&A: The market is consolidating through landmark digital infrastructure transactions, such as the KKR and Singtel acquisition of ST Telemedia Global Data Centres (STT GDC). This M&A activity is explicitly driven by the need to secure and scale multi-gigawatt capacity (STT GDC has 2.3 GW) to meet the massive demand from hyperscalers deploying GPU clusters.

In conclusion, global AI data center construction and investment activities represent a strategic, capital-intensive race to establish the physical foundation of the AI economy. Success hinges on mastering complex engineering (high-density power and liquid cooling) and forging strategic partnerships that bridge the worlds of utilities, national infrastructure, and cutting-edge silicon.

Side Note:

While the entire world seems glued to Nvidia’s daily stock chart and the endless media circus surrounding it, the real action has been quietly compounding in the “boring” plumbing of the data center supply chain—specifically the power sector. Case in point: Fortune Electric (1519 TPE) has surged a staggering ~30x since 2023, leaving even Nvidia’s impressive 11x run in the dust.

That is the thrill of the hunt—digging past the headlines to find those hidden gems where the returns are truly astronomical.

That is exactly our mission at this Substack: we sift through the chaotic, unstructured data to find the signal for you. We aren’t financial advisors and this isn’t a buy recommendation, but let this be a reminder that the AI boom is massive, and the biggest winners aren’t always the ones on the front page.

Disclaimer: This document presents proprietary industry research and analysis. The projections and conclusions contained herein are for informational purposes only and should not be construed as investment recommendations or financial advice in any form. We aim to provide factual information combined with our independent analysis to enhance the reader’s understanding of the technology industry.